Key Takeaways

- Historical data suggests that the real market impact often comes years after an IPO, when lock-up periods expire and insiders begin selling.

- Goldman Sachs research shows that companies with very low initial free floats tend to dramatically increase the number of shares available to the market over time.

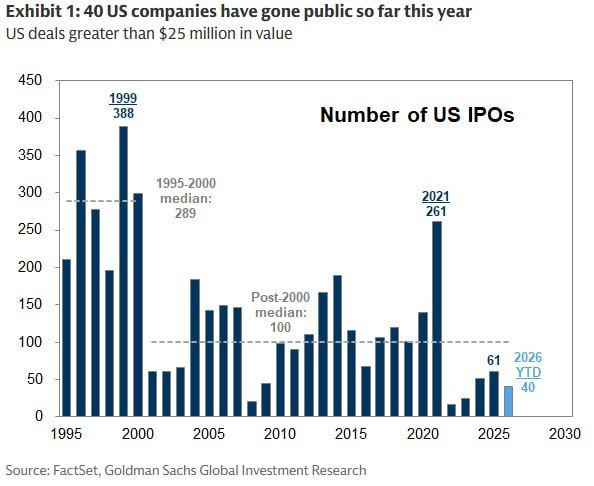

- The dot-com era provides a cautionary example: IPO activity peaked in 1999, while the market topped and crashed in 2000 as insider shares flooded the market.

- Arthur Hayes recently closed his entire HYPE and NEAR positions, citing upcoming AI mega-IPOs as one reason for raising liquidity ahead of what he expects to be a major market transition.

The Next Great IPO Cycle Is Coming

Investors are increasingly focused on a new generation of highly anticipated public listings. Companies such as SpaceX, Anthropic, OpenAI, Databricks, Stripe, and several other private giants are widely expected to pursue public offerings over the coming years.

These potential listings could collectively represent hundreds of billions of dollars in market capitalization entering public markets. While IPOs are generally viewed as a sign of healthy capital markets and growing investor appetite, they also raise an important question:

Will this unprecedented wave of IPOs eventually overwhelm the stock market?

According to Bloomberg columnist John Authers, the answer is probably not – at least not initially.

Why Investors Are Concerned

The fear is rooted in a simple principle that governs all markets: supply and demand.

All else being equal, a sharp increase in the supply of shares should put downward pressure on prices. The scale of new equity supply that may arrive over the next several years is extraordinary, and the impact extends far beyond the IPO event itself.

Many of today's private technology giants are expected to debut with relatively small free floats, meaning only a limited portion of their shares will be available for public trading. However, history shows that this changes rapidly over time.

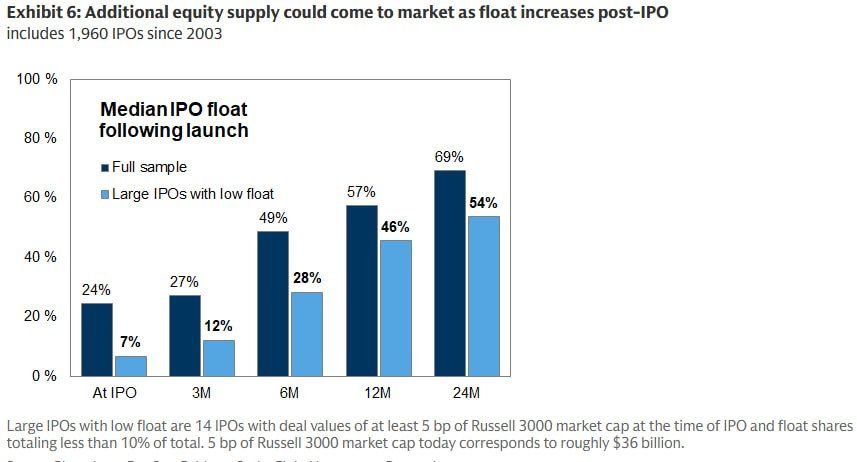

What Goldman Sachs Research Reveals

Research from Goldman Sachs found that large companies that listed with extremely low free floats — 7% or less at IPO — typically expanded their publicly tradable share base to approximately 54% within two years.

Across the broader IPO sample, companies that debuted with an average free float of 24% saw that figure rise to roughly 69% within 24 months.

In other words, the IPO itself is often only the beginning of the supply story.

As lock-up periods expire and early investors, founders, and employees gain the ability to sell their holdings, millions — and sometimes billions — of additional shares can enter the market.

The Dot-Com Lesson

History offers a clear warning.

During the dot-com boom, IPO issuance peaked in 1999. However, the broader stock market did not reach its ultimate peak until the following year.

As lock-up restrictions expired, founders and early investors rushed to monetize their gains, dramatically increasing share supply. The resulting wave of selling coincided with one of the most severe market downturns in modern history.

The lesson is that the greatest pressure from IPOs may not occur during the initial listing frenzy but rather in the years that follow.

Why 2027–2028 Could Matter More Than 2026

If companies such as SpaceX, Anthropic, OpenAI, and other private technology leaders follow historical patterns, the real challenge for markets may emerge one to two years after their IPOs.

The initial listings could be absorbed relatively smoothly by investor demand. However, as insider lock-ups expire and free floats expand, the cumulative weight of new shares could become substantial.

That suggests the period around 2027–2028 may be more important for investors to monitor than the IPO announcements themselves.

Arthur Hayes Is Already Positioning for the Shift

This broader theme may help explain recent positioning changes by prominent macro investor Arthur Hayes.

According to Cointelegraph, Hayes has exited his entire HYPE and NEAR positions, citing rising energy prices, the coming wave of AI mega-IPOs, and his expectation that markets could reach a cyclical high before September.

The move signals a desire to increase liquidity ahead of what could become one of the largest capital-allocation events of the decade. If major AI and technology IPOs begin attracting institutional capital, investors may increasingly rotate funds away from risk assets and toward newly listed market leaders.

Whether or not the IPO wave ultimately triggers a broader market correction, one thing is clear: the coming years could bring an unprecedented transfer of capital as some of the world's most valuable private companies finally enter public markets.